From Ratings to ECL: How to measure IFRS9 metrics.

Under IFRS 9, banks are required to calculate Expected Credit Losses (ECL) using forward-looking information rather than relying purely on historical loss experience. The process can be broken down into clear, sequential steps:

1. Internal Rating and TTC PD Calibration

a) Internal Rating Assignment

Each borrower must be assigned an internal credit rating.

Ratings can be derived using internal models or credit scoring systems that consider financials, qualitative factors, and external ratings (if available).

b) Historical Default Rate Estimation

For each segment (e.g., corporate, retail, SME), compute long-run observed default frequencies.

Map these historical default rates to rating buckets (AAA, AA, A, BBB, etc.) to produce Through-the-Cycle (TTC) PDs.

c) TTC PD Calibration

Adjust observed default frequencies to remove short-term cyclical effects.

Ensure that long-term PDs add up to historical default experience (back-testing is required).

Map TTC PDs back to each client’s internal rating — this is the baseline probability of default.

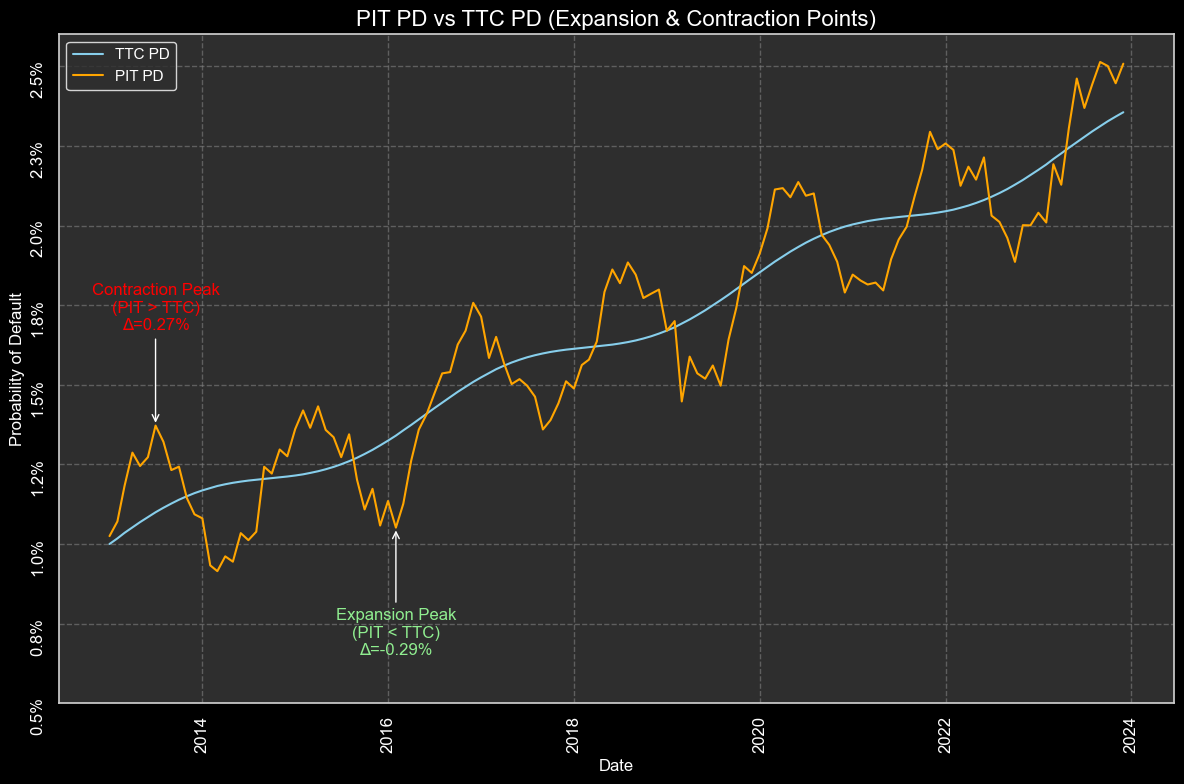

2. Macroeconomic Impact (TTC → PIT PD)

a) Macro-economic Overlay / Satellite Models

TTC PD serves as the anchor.

Use regression, probit, or machine-learning models to estimate macro sensitivity of each segment/rating to key drivers:

GDP growth

Unemployment

Interest rates

Inflation

Sector-specific indices

b) PIT PD Calculation

Apply current macro-economic data or scenario projections to adjust TTC PD upward or downward.

Generate forward-looking PIT PDs for:

Base scenario

Upside scenario

Downside scenario

Apply the probability-weighted average of these scenarios to derive the final PIT PD for ECL purposes.

3. LGD (Loss Given Default)

a) Portfolio Segmentation

Split the portfolio into secured vs unsecured exposures.

b) LGD Estimation

For secured exposures, calculate recovery rates based on:

Updated collateral values (haircut for market volatility)

Legal and workout costs

Discount factors to present value

For unsecured exposures, use:

Historical recovery experience

Sector-specific loss data

Adjustments for economic outlook

c) PIT LGD (if material)

Some banks adjust LGD based on macro conditions (e.g., real estate downturn reduces recovery rates).

4. EAD (Exposure at Default)

a) Current Exposure

Capture the on-balance sheet exposure (loans outstanding).

b) Off-Balance Sheet Conversion

Apply Credit Conversion Factors (CCFs) for undrawn commitments, guarantees, letters of credit, etc.

Estimate expected exposure at the point of default.

5. Discounting and Maturity Adjustment

Effective Interest Rate (EIR) Application: Apply the Effective Interest Rate (EIR) to discount expected losses, reflecting the time value of money, to their present value.

Projection Horizon: For Stage 1 exposures, project Probability of Default (PDt), Loss Given Default (LGDt), and Exposure at Default (EADt) over a 12-month horizon (t=1 year) for the calculation of 12-month ECL. For Stage 2 and all Stage 3 sub-categories (3.a, 3.b, 3.c) exposures, project PDt, LGDt, and EADt over the remaining contractual life of the asset for the calculation of Lifetime ECL. This aligns with the forward-looking nature of IFRS 9 and CBUAE requirements.

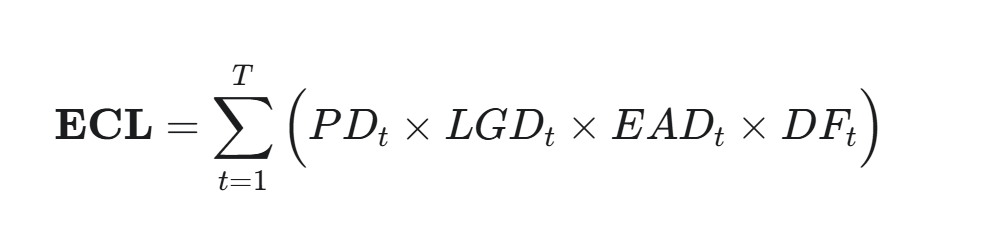

6. Final ECL Calculation

The final Expected Credit Loss (ECL) is calculated as the sum of discounted expected losses over the appropriate time horizon:

Where:

PD_t: Forward-looking Point-in-Time (PIT) probability of default at time t, incorporating macroeconomic scenarios and meeting the CBUAE's proactive assessment requirements.

LGD_t: Loss Given Default, reflecting the proportion of exposure that will not be recovered, considering secured/unsecured recovery rates.

EAD_t: Exposure at Default, encompassing both on-balance sheet and off-balance sheet exposures, consistent with CBUAE guidelines.

DF_t: Discount Factor, based on the Effective Interest Rate (EIR), to bring future expected losses to present value.

Application Horizon based on Stages:

For Stage 1 assets: Utilize 12-month ECL (T=1 year).

For Stage 2 and all Stage 3 assets (3.a, 3.b, 3.c): Utilize Lifetime ECL (T = remaining life of the facility), reflecting the increased risk profile and the CBUAE's emphasis on comprehensive provisioning for impaired assets.